Australia’s Consumer Data Right to open banking

by Doug Morris, CEO, Sharesight

In collaboration with Fintech Australia, Sharesight has officially endorsed a submission on the Treasury Laws Amendment (Consumer Data Right) Bill 2019 that seeks to create the Consumer Data Right (CDR) with an amendment to the Competition and Consumer Act 2010.

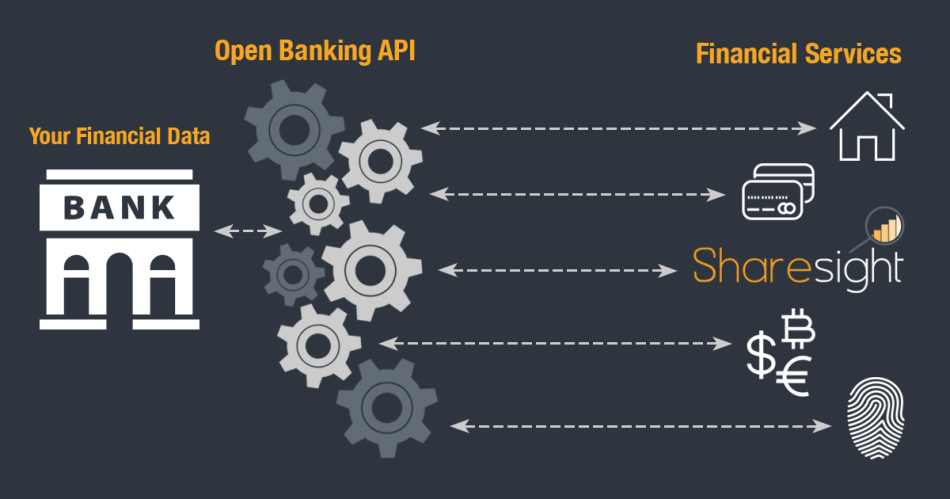

The Consumer Data Right (CDR) will mandate that banks and financial institutions (before later extending to telecommunications and utility providers) make it easy, safe, and practical for consumers to share their data with third parties — including competing services. It’s one of several critical ingredients needed to improve the financial outcome for Australians. Open Banking initiatives are already in place in the UK, and progress is being made in Canada and New Zealand.

Banks hate the CDR

Many countries (Australia especially) have banking oligopolies, and no one wants to be responsible for killing the golden goose. Banks know that keeping clients inside their walled gardens is key to revenue growth by upselling them products like financial advice and mortgages. Just this week, I opened a “high” interest savings account with my incumbent bank in literally 3 mouse clicks — it works.

Historically, banks benefited from the fact that switching was way too painful for the average client. Open Banking threatens that because it builds the plumbing required to make switching easy. It will be like signing into something with your Google account. Ironically, banks have only come to understand that customer data is an asset once fintechs build clever ways of extracting that data.

Consumer data right is progress

We’re excited about the progress made. Eventually, Open Banking will make it easier for you to control access to your online brokerage and share registry data, which in turn means more investors can shop for better services, and use software solutions like Sharesight. This is a relatively minor use case. Open Banking could eventually have mass impact on the superannuation and everyday banking markets.

CDR legislation is only the first step

The CDR is not a panacea. The old saying in software goes, 80% of people use 20% of your product. I’d argue that ratio will be more like 98% to 2% when Open Banking debuts.

I don’t mean to throw cold water on an initiative we believe in. But think about it this way: If I bury a feature within a settings menu, and that settings menu lives within an advanced settings menu, which lives in a system preferences menu… how many people will be motivated to seek this feature out? The banks will bury their government-mandated Open Banking settings the same way.

The key to making this work is financial education. Yes, fintechs provide better alternatives, but missing is the broad consumer demand and knowledge that challenger companies will save them money.