6 lessons from the Gamestop saga

By Damien Klassen is Head of Investments at Nucleus Wealth.

There has been a lot written about the Gamestop saga in the last week. I want to discuss the medium-term market impacts rather than moralising about who is right and wrong. While I doubt it marks the top of the current market, there are some concerning signs.

Quick background

The wallstreetbets forum on Reddit spawned several short squeeze raids on stocks. The highest-profile was Gamestop where hedge fund short sellers lost billions, individual investors made (and in many cases lost) millions.

The concept of a short squeeze is not new.

The new part was the organisation of thousands of small investors to participate. Also, some sophisticated manipulation of the options market added to the upside.

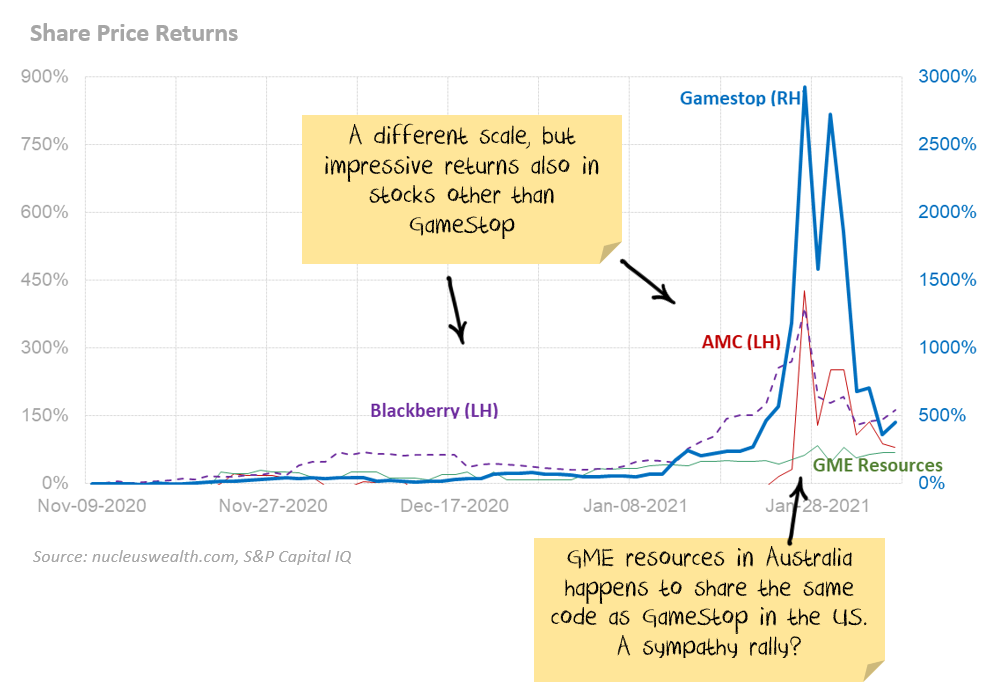

The poster-child short squeeze target was Gamestop. But there were plenty of other companies with similarly poor fundamentals and excess of short-sellers, making them vulnerable.

Lesson 1. Short-sellers: Fundamental problems?

Has this episode illustrated the fundamental problems with short selling?

In many ways, yes. But these issues have always been there.

Short selling is very different from buying a stock:

- When an investor buys a stock, there are no further obligations. They cannot lose any more. If the stock goes down, it becomes a smaller weight in the portfolio and therefore, less of a problem.

- When an investor shorts a stock, they promise to return the stock in the future. The investor needs to post collateral and can lose significantly more. If the stock goes up, it becomes a bigger weight in the portfolio and therefore, more of a problem.

I think of investors as being price-sensitive or not. i.e. does valuation matter or is it only the story. For a short-seller, the price-insensitive investor is the enemy:

- A value investor might have bought Gamestop at $5 with a bullish thesis. But at $20 they are likely to be selling. At $400, the value investor is long gone.

- For the price-insensitive investor, there is little difference. For some, they are more likely to be buying at $400 because the price rise has “proven” the story.

The Reddit crowd (despite the ringleader calling himself deepf#$%ingvalue) have clearly been price insensitive.

Shorting usually reduces volatility as it provides a counterbalance to price-insensitive buyers. But, at certain levels, it reverses and makes the volatility exponentially higher. For example:

- Say we add a new price-insensitive buyer and add a new short seller. Their positions cancel. The stock price doesn’t move because there are no shares needed.

- However, if we add 50 new price-insensitive buyers, the stock price is forced up. Then some of the shorts need to buy back their positions to reduce risk. Which forces the price even further up.

The net effect is the potential threat of future flash-mobs will change behaviour for short-sellers.

Short-selling: likely trends

Shorting illiquid stocks will be significantly curtailed for risk reasons. There will be fewer shorts. Crowded shorts will be less likely.

There will likely be outflows from managers which will reduce the size of the sector. And fewer funds will likely improve returns for the remaining players.

Will this cause problems for the market? Probably not at a headline level. Most funds that are short also have stocks that they own to offset the short. These are called long/short funds. Most long/short funds will buy back their shorts on one hand while selling their longs on the other.

There will be an effect on individual stocks. Often it will be low-quality stocks rising (these are the ones shorted) and higher quality stocks falling.

Keep in mind that some of this has already happened. Press reports of other highly shorted stocks rising because of Reddit raids are likely only partly true. The other part of the stock price rise is likely to be short sellers closing vulnerable positions. Voluntarily for risk control, or involuntarily due to withdrawals or prime broker risk measures.

Lesson 2. Options markets: Exploiting flaws

Sophisticated option buying aided the share price gains. Called a gamma squeeze, it involved buying:

- Deep out of the money options. These provide extreme upside to the buyer if the share price rose.

- At the money options. This forces market makers to buy shares to hedge. This action drove the share price higher.

Done in enough size, it super-charged the returns far more than buying the same dollar amount of ordinary shares.

Options market: likely trends

Pre-1987, investors were using a technique called portfolio insurance to hedge their portfolios. In the 1987 crash, it didn’t work. The price of put options (which did work) become structurally higher after this event.

Market makers don’t like to lose money. So, I’m expecting structurally higher call option prices for stocks. Especially for smaller, less liquid stocks. And also for any stocks with considerable short selling.

This is a mild negative for the market. But probably more than offset by other factors. It will also limit the effectiveness of similar trades in the future because the perpetrators won’t get as much leverage.

Lesson 3. Retail Traders: When the product is free, you are the product

Many of the traders have been using “free” trading systems like Robinhood and “free” research on Reddit.

The issue with free trading is that the traders using this are not the customer – the traders are in fact the product. Robinhood makes money through providing trading flows and data to hedge funds, and through stock lending.

Conspiracy theories are floating around about how Robinhood (and others) manipulated the markets. This meant their real clients, hedge funds, could exit positions. In my view, there is more credibility to the official explanation: the stocks were so volatile that counterparties demanded more collateral. Robinhood raised billions of dollars to meet obligations over a few days. Which further suggests the official explanation is the truth. But we may never know.

Secondly, some of the free research from Reddit looks awfully sophisticated. And the advice to “holding on to stick it to the hedge funds” doesn’t seem in investors’ best interest. Is it possible professional traders are trying to weaponise retail traders? Absolutely. If not before, then Gamestop has undoubtedly provided a template for the future.

As Gamestop was squeezed up, hedge funds clearly lost a lot of money. But it will be the retail traders that have lost out on the way down.

Finally, and perhaps most importantly, this episode has “proven” trading can produce lottery-type returns. i.e. the expected value of each ticket is negative, but an enormous payoff and a chance to dream is possible. It is probably going to attract new investors.

Retail traders: likely trends

Free brokerages will spend a while in the public relations doghouse, and maybe some larger clients will go to paid services. But free is free. I’m expecting the lottery ticket perception will probably mean more trading at Robinhood.

Pseudonymous authors will swamp Reddit, talking their book. This “free” advice will not help the average retail trader.

We are in a liquidity-driven share price boom, which I don’t think is sustainable. But there is still a lot of government and central bank stimulus. And retail investors have just been given proof of lottery-like returns. So there will likely be more of them.

Lesson 4. Prime brokers: financial market plumbing

Prime brokers sit behind many hedge funds, providing them with the capital to trade. They let hedge funds use debt to increase the possible returns greatly. Which also dramatically increases the risks.

There are a lot of hedge funds which lost a lot of money in January. Melvin Capital lost over 50%. Risk controls at prime brokers are going to be important once again.

Prime brokers: likely trends

Prime brokers will scale back lending in the short term. This is a risk to markets if the scale back is significant.

I suspect within months, lending won’t be affected that much. And the lessons learned by prime brokers will probably be:

- individual stock risk controls are more important

- but there were no massive blow-ups to threaten the system

- and Robinhood managed to raise a lot of money in the middle of the crisis to avert problems

- therefore business as usual

I‘m not sure this is the right lesson to learn. But it will probably be the lesson learned.

Lesson 5. Exchange-Traded Fund composition: buyer beware

Exchange-traded funds (ETFs) have become very large in recent years. These funds have strict rules. In episodes like these, some funds become unbalanced.

Gamestop at one point was over 22% of the SPDR S&P Retail fund. Even more concerningly, an investor in the Invesco Smallcap value fund would have received get a 16%+ exposure to a single loss-making stock trading on a massive price to sales ratio. There are a lot of other examples where Gamestop became a disturbingly large holding. Buyer beware.

Second, there is debate whether the explosive growth in exchange-traded funds is increasing volatility in prices. I’m going to sidestep that question today because it is a long answer. What I will posit is:

- When traders look at short interest to work out whether there can be a short squeeze, they exclude large strategic shareholders.

- Given exchange-traded funds are price-insensitive, they should be treated like strategic shareholders.

Lesson 6. Markets are pumped up with debt and stimulus; weird stuff is going to continue

Share markets are at extreme valuations on the back of stimulus, hope, retail trading debt and derivatives. Fundamental valuations are difficult at the moment which, for some, is a good excuse to ignore them.

Weird stuff is going to keep happening. However, the next one won’t look like Gamestop. The market has been put on notice about the dangers and is unlikely to make the same mistake again. Scratch that. It will definitely make that same mistake again, but not for a few years. The next event will be different.

The market’s financial plumbing was not built for incredibly volatile day-to-day movements, extreme leverage, a host of price-insensitive buyers, and record levels of option buying.

The financial plumbing will be tested again.

I’m not expecting it to crack, but investors need to be aware that it might. When markets are no longer based on capitalism, but propped up on government and central bank support, then the biggest risk remains policy error in response to one of these tests.